Over the next two decades, more than US$15 trillion in wealth is expected to transfer from Baby Boomers to their children and grandchildren. In New Zealand, this seismic shift is already underway. Yet, as discussed in FNZ's recent webinar, The Future of Wealth in New Zealand, many wealth advisors and firms are not equipped to engage this emerging cohort effectively. The younger generation isn't just a future growth market—it's an urgent opportunity for firms seeking long-term relevance.

To capitalise on this shift, financial institutions must fundamentally rethink how they engage the next generation. This is not a matter of rebranding brochures or building token digital tools. It is about redesigning the entire engagement model to align with the expectations, behaviours, and values of a digitally native, socially conscious, and time-poor generation.

1. Understand where and how younger investors engage

Gen Z and Millennials interact with the world differently than their predecessors. They are mobile-first, digitally fluent, and accustomed to on-demand experiences tailored to their needs. According to insights shared in the webinar, younger investors expect investment platforms to be intuitive, accessible, and interactive. They favour channels that reflect their lifestyles: apps over desktops, stories over documents, push notifications over phone calls.

Importantly, this cohort often begins their investment journey without human advisors. They rely on peer recommendations, online reviews, podcasts, YouTube, and increasingly, influencers on social platforms like TikTok and Instagram. Financial institutions that dismiss these new channels as fads are missing the point. This is where trust is being built, narratives are being shaped, and decisions are being influenced.

To remain relevant, traditional advisors must meet younger investors where they already are—and do so authentically.

2. Reframe financial advice as ongoing, shared experience

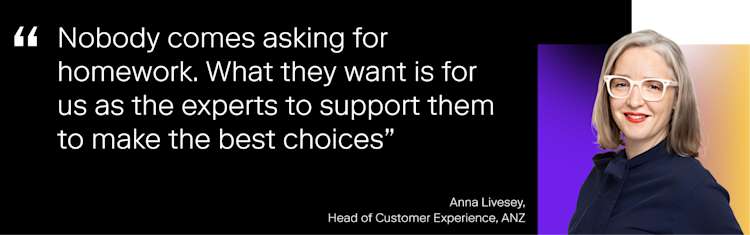

One of the most telling insights from the webinar came from Anna Livesey of ANZ, who highlighted that young customers are not looking for "homework" from their financial institutions.

This reframes the role of advice from a periodic, transactional engagement to a shared journey. Technology plays a pivotal role here. Tools that visualise trade-offs, simulate future outcomes, or simplify contribution changes can create a sense of empowerment.

But design isn't everything. If the interface is clunky, the language patronising, or the tone unrelatable, the opportunity is lost. Institutions must invest in user experience research, behavioural science, and inclusive design if they are serious about connecting with younger generations.

3. Embrace hybrid models

The notion that digital tools will replace human advice is false. As several panellists noted, trust remains a cornerstone of financial decision-making, especially in uncertain times.

What younger investors want is not a choice between human and digital, but the ability to navigate both seamlessly. A digital-first experience that includes the option for human support at critical moments. Or human advisors empowered by AI tools that allow them to deliver highly personalised advice at scale.

Firms should design their engagement models around customer intent, not internal operational silos. This means enabling transitions between channels that feel natural and maintaining context across interactions. If a user moves from a budgeting app to a live chat with an advisor, the experience should be continuous and coherent.

4. Make values-based investing real and relevant

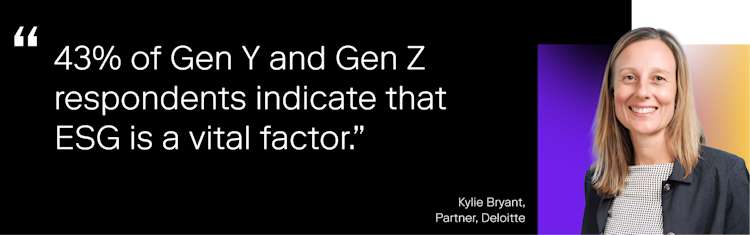

As highlighted in the webinar, ESG (Environmental, Social, and Governance) factors are increasingly influential, particularly among Gen Z and Millennials. Yet the industry often mishandles this demand—either over-marketing generic ESG products or underestimating the sophistication of this audience.

Compared to older generations who prioritise income and lifestyle preservation.

Younger investors want to see how their investments align with their values. They want transparency, not greenwashing. And they want choice, not a one-size-fits-all ESG fund. Providers that can offer clear data, actionable insights, and meaningful customisation will win trust.

This means going beyond product labelling to include tools that show portfolio impact, ESG score explanations, and even the ability to exclude specific sectors. Crucially, it also means being honest about trade-offs and limitations.

5. Foster financial literacy through embedded learning

Financial literacy is still a major barrier for younger generations, especially as investing becomes more accessible. But as several webinar panellists noted, today's young adults don’t want to be taught in the traditional sense. They want to learn by doing, guided by intuitive tools and social proof.

This opens up an opportunity for embedded education—learning that happens naturally within the context of a user’s journey. For example, explaining volatility while selecting a fund, or illustrating the long-term impact of compounding when adjusting contribution rates.

The key is timing and tone. Educational nudges should feel helpful, not intrusive; empowering, not preachy. And they should always be optional, allowing users to engage more deeply when they feel ready.

6. Reimagine customer segmentation and lifecycle models

Traditional segmentation models based on age, wealth, or product holdings are no longer sufficient. As panellist Kylie Bryant of Deloitte noted, customer segmentation must evolve to reflect values, digital behaviours, and life moments.

This underscores the need for dynamic, multi-dimensional segmentation approaches.

This means moving from a static view of "customer types" to a dynamic understanding of needs. A 25-year-old freelancer saving for their first home will have very different needs from a 25-year-old entrepreneur scaling their start-up. Yet many financial institutions treat them the same.

Advanced data analytics, machine learning, and user journey mapping can help create more nuanced personas. But to be effective, this insight must be operationalised into the design of products, communications, and support models.

7. Build trust through transparency and inclusion

Younger generations are deeply sceptical of institutions. They demand transparency, value diversity, and expect brands to take a stand on social issues.

Trust must be earned through consistent, inclusive, and transparent practices. This includes clear fee structures, plain language explanations, inclusive imagery and messaging, and visible commitments to ESG and DEI.

Firms that prioritise these principles in both internal culture and external communications will be better positioned to build lasting relationships with younger investors.

Conclusion: The future of wealth is not a future problem

It is a present imperative. As the webinar made clear, the demographic, technological, and cultural forces reshaping the industry are already in motion. Financial institutions that act now to engage the next generation authentically, holistically, and digitally will not only capture market share—they will shape the future of the industry.

Those that fail to evolve risk becoming irrelevant to the very cohort that will soon control the majority of global wealth.

Rethinking engagement is not optional. It is the strategy.

Jeremy Graham

Head of Technology Asia Pacific, Middle East and Africa