How it all began

The 2008 global financial crisis will be remembered as one of the most significant events in recent history, not just for the downward impact it had on stock markets around the world, but also for the aftermath that followed. Central banks devised unorthodox measures to increase money supply in the economy, which inadvertently pushed up prices across all asset classes. Governments had to bail out major financial institutions whilst introducing a flurry of new regulations to avoid the repeat of the crisis. Consumer trust in financial services providers reached an all-time low, and many felt the pinch of stagnating wages combined with inflationary pressures on purchasing power.

This new global environment, along with the growth in the use of smartphones and tablets, planted the seeds for the perfect storm within the Financial sector – what is now known as FinTech, the popularised term for Financial Technology. This has resulted in increasing levels of focus and investment in this emerging space from corporates, private equity and venture capital.

Source: The Pulse of FinTech 2018, KPMG International (data provided by Pitchbook

Fintech verticals

The FinTech landscape can be divided into several different sub-segments, which mostly corresponds to that of the wider Financial sector.

Payments and transactions

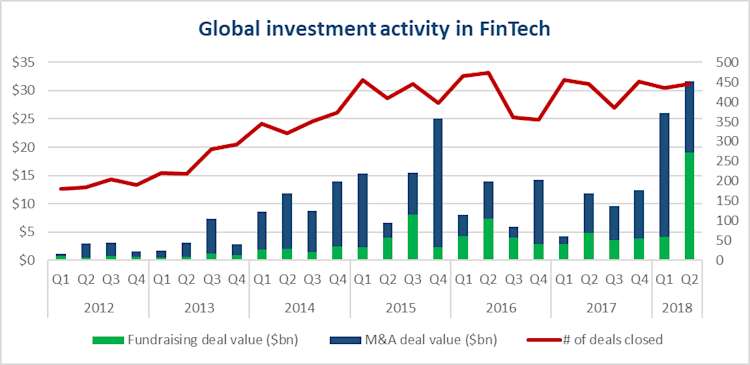

The Payments sector is one of the largest FinTech verticals in terms of revenue. Reflecting the maturity of this sector, the first half of 2018 saw the acquisitions of WorldPay (£9.3bn) and iZettle ($2.2bn) by Vantiv and PayPal respectively. New regulations in the form of the PSD2 and Open Banking is expected to foster further innovation and opportunities within this sector.

Lending

Stricter regulatory capital requirements post-financial crisis caused many banks to tighten their lending, which resulted in a funding gap for retail consumers as well as SMEs. This subsequently led to the rise of alternative credit providers, such as P2P and crowdfunding lenders RateSetter and Funding Circle, with the latter planning to complete an IPO this year.

Banking

Following the financial crisis, the UK government encouraged the development of ‘challenger banks’ to foster competition and help address areas underserved by the larger banks. The first half of 2018 has seen successful fundraisings by Revolut ($250m), Atom Bank ($207m) and N26 ($160m).

The world is being transformed by a technological revolution…FinTech promises to change the way we bank, invest, insure and even pay for things.

Wealth and asset management (WealthTech)

The wealth and asset management sector has seen many changes in the UK since the financial crisis, be it through process compliance requirements (eg. RDR, MIFID II) or changes in personal financial and tax rules (eg. Pension Freedoms).

This has led to a mass adoption of technology, mainly in the form of wealth platforms, to support processes that meet new regulatory requirements and service propositions. FNZ has played a key role in serving these needs, by partnering with major financial institutions to enable them to provide the latest WealthTech services to their clients.

Insurance (InsurTech)

The InsurTech sector is fairly nascent compared to its other FinTech counterparts. There have been many new entrants into this space, playing the roles of product aggregators, insurance managers, P2P intermediaries and direct insurers – however the Insurance sector remains difficult to disrupt. Cyber security insurance has been a notable new area of early-stage FinTech investing following increased demand in this type of protection. The first half of 2018 saw investments in Oscar Health ($165m) and Lemonade ($120m) led by Founders Fund and Softbank respectively.

Regulatory (RegTech)

The Financial sector is very regulatory driven, and investment in this area of FinTech has seen a pickup in the past year following the introductions of various new regulations – Dodd-Frank in the US and PSD2, MIFID II, MIFIR and GDPR in Europe.

Emerging Technologies

There are several main technologies currently emerging within the FinTech space:

Data-Focused | Front-End Interface | Operations | Infrastructure |

|---|---|---|---|

Analytics AI and machine learning Sensor-based technology Biometrics | Intuitive user interface Gamification Augmented and virtual reality | Robotic process automation Chatbots Blockchain and DLT | Platformification Cloud Open APIs |

Source: Capgemini World FinTech Report 2018

Data-Focussed

The use of predictive analytics via machine learning enables companies to make better recommendations to consumers based on their own historic behaviour or that of other consumers with similar backgrounds. Read more about our approach to Predictive Analytics

Front-End Interface

Improvements in front-end interfaces enable increased customer engagement. For example, the WealthTech start-up Advicefront has developed a slick onboarding interface for what is normally a time-consuming process for financial advisers and their clients. Read more

Operations

Increased efficiency in operations can create significant cost-savings for the product provider, which in turn results in lower costs for the end consumer. Blockchain or DLT in particular has the potential to eliminate transaction reconciliation errors between two or more financial institutions by creating a single shared ledger of records. Read more about the Blockchain Revolution at FNZ.

Infrastructure

Open APIs allow for the sharing of data points between two or more different software or web service, enabling the appearance of a single platform of services for the end user.

Future trends

One of the main challenges for FinTech start-ups is achieving scale and profitability. It is therefore anticipated that further consolidation of the market will occur as it continues to mature, with more M&A deals predicted in the near future.

Governments and regulators are also expected to continue to introduce policies that promote innovation within the Financial sector. The UK has been leading the way with its much-emulated Regulatory Sandbox concept, and its implementation of Open Banking is now also being replicated across the globe.

More partnerships between major financial institutions and FinTech providers are likely to take place, as each party look to leverage the strengths of the other whilst sharing their own. This can only result in a win-win-win situation; for the financial institution, the FinTech provider and – most importantly – the end consumer.